Savings vs Investment: Key Differences for Indian Families

Understand the difference between savings and investment. Learn how to grow wealth, manage risks, and plan your financial future with Nila Safe Life Solutions.

FINANCIAL PLANNING

Sundari S Mahila Career Advisor – LIC Tindivanam

4/10/20265 min read

Savings vs Investment: The Ultimate Guide to Building Wealth for Indian Families

Language: தமிழ் | English

Introduction

Every Indian household has a tradition of "saving." From the spare change kept in kitchen containers to the disciplined monthly deposits in a bank account, we are a nation of savers. However, in today’s economy, simply saving money is no longer enough to secure your children’s education, their marriage, or your own peaceful retirement.

To truly achieve financial freedom, you must understand the logic of savings vs. investments. While they are often used interchangeably, there is a significant difference between savings and investment. Knowing when to save and when to invest is the secret to successful financial planning.

In this comprehensive guide, we will break down the savings definition, the investment definition, and how you can use wealth-building strategies to secure your family's future with Nila Safe Life Solutions.

What is Savings? (The Savings Definition)

Savings refers to the portion of your income that you do not spend. It is money set aside for future use, usually held in highly liquid, safe accounts.

Key Characteristics of Savings:

Liquidity: You can access your money almost instantly.

Safety: There is virtually no risk of losing your principal amount.

Low Returns: The interest earned on a standard savings account is often lower than the inflation rate.

Purpose: Savings are best suited for short-term goals and emergencies.

What is Investment? (The Investment Definition)

Investment is the process of putting your savings into financial products or assets with the expectation that they will grow over time. Unlike savings, investments are designed to generate a higher return.

Key Characteristics of Investment:

Growth Potential: The primary goal is to build wealth over the long term.

Risk Factor: Investing carries more risk than saving, as asset values can fluctuate.

Compounding: Investments benefit from the power of compounding, where your earnings generate their own earnings.

Purpose: Investments are used to achieve long-term financial goals, such as buying a home or saving for retirement.

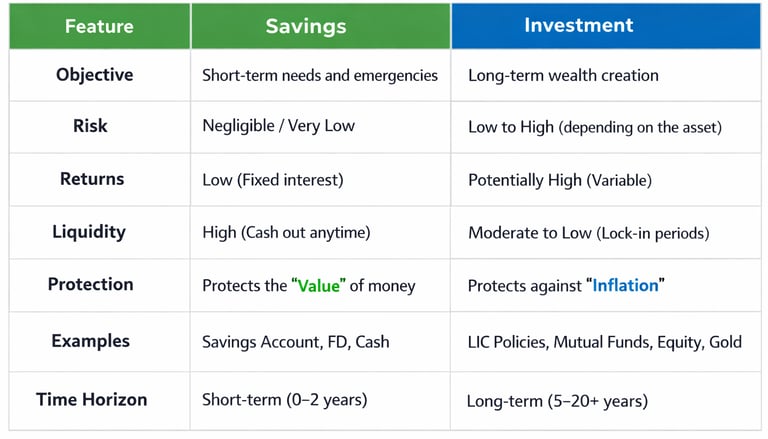

Savings vs Investment: 7 Key Differences You Must Know

Understanding the difference between savings and

investment is easier when comparing them side by side.

Why This Topic is Important for Indian Families

For Indian middle-class families, the cost of living is rising every year. This is called inflation. If you keep all your money in a traditional savings account, the rising cost of petrol, school fees, and groceries will eventually eat into your purchasing power.

1. Beating Inflation

Inflation in India usually hovers around 5-6%. If your savings account gives you 3% interest, you are actually losing money every year. Investment options such as LIC plans and diversified portfolios can help you earn returns that beat inflation.

2. Meeting Life Milestones

Whether it is a daughter's wedding or a son's higher education abroad, these milestones require a large "corpus" (a big sum of money). You cannot build a 50-lakh corpus just by saving; you need the benefits of investment to multiply your capital.

3. Emergency Preparedness

While investments grow your wealth, savings keep you afloat during a crisis. Having an emergency fund ensures that you don’t have to break your long-term investments if there is a sudden medical emergency or job loss.

Step-by-Step Financial Planning Guide

As a financial advisor at Nila Safe Life Solutions, I recommend this step-by-step approach to balance your savings vs investment needs.

Step 1: Create a Budget

Track your monthly income and expenses. Aim to save at least 20% of your take-home pay.

Step 2: Build an Emergency Fund

Before you start investing, keep 6 months’ worth of expenses in a savings account. This provides peace of mind.

Step 3: Secure Your Family with Insurance

This is the most critical step in financial planning basics. Before looking for high returns, ensure you have a Term Insurance or an LIC Life Insurance policy. This protects your family’s lifestyle if the breadwinner is no longer there.

Step 4: Define Your Goals

Divide your goals into long-term vs short-term financial goals.

Short-term: New car, vacation, home renovation (Save for these).

Long-term: Retirement, child’s education (Invest for these).

Step 5: Diversify Your Portfolio

Don't put all your eggs in one basket. Mix safe instruments such as LIC policies and Fixed Deposits with growth-oriented assets like Mutual Funds or Equity.

Practical Savings vs Investment Examples for Indian Families

Let’s look at two scenarios for a typical salaried employee in India earning ₹60,000 per month.

Scenario A: The "Only Saver"

Ramesh saves ₹15,000 every month in a standard savings account for 20 years.

Result: He has a safe amount of money, but the total value is barely enough to cover his daughter’s college fees because inflation has made education 3 times more expensive.

Scenario B: The "Smart Investor"

Suresh saves ₹5,000 for emergencies and invests ₹10,000 in a combination of an LIC Wealth Plan and a Diversified Fund.

Result: Over 20 years, the power of compounding works its magic. Suresh not only has money for his daughter's education but also a significant fund for his own retirement.

Common Financial Mistakes to Avoid

Ignoring Insurance: Many people treat insurance as an expense. In reality, it is the foundation of your wealth-building strategies.

Starting Too Late: The longer you wait to invest, the more you lose out on the power of compounding.

Mixing Liquidity with Growth: Keeping too much money in a savings account (where it doesn't grow) or locking all your money in long-term assets (where you can't touch it during an emergency).

Chasing "Get Rich Quick" Schemes: Avoid high-risk, unregulated schemes. Stick to trusted institutions like LIC.

Financial Planning Tips from Your Advisor

As a Mahila Career Agent – LIC Tindivanam, I have helped many families in and around Tindivanam secure their future. Here are my top tips:

Automate Your Investments: Set up a mandate so your LIC premium or investment amount is deducted as soon as your salary is credited.

Review Yearly: Your financial needs change when you get married or have a child. Review your plan at least once a year.

"Focus on Tax Savings: Utilise sections such as 80C to save on taxes while investing in LIC policies.

Think Long-Term: Don't get worried by daily market news. Patience is the key to investment success.

FAQ Section

1. Which is better, savings or investment?

Neither is "better" than the other; they serve different purposes. Savings provide security and liquidity for the short term, while investments provide growth for the long term. A healthy financial plan needs both.

2. Is LIC a savings or an investment?

LIC policies often offer a unique blend of both. They provide the safety and discipline of savings with the life cover and long-term growth of an investment.

3. How much of my salary should I invest?

A general rule of thumb is the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and investments.

4. What are the safest investment options in India?

The Public Provident Fund (PPF), National Savings Certificate (NSC), and LIC insurance policies are considered among the safest investments because the Indian government backs them or has a long history of trust.

5. Can I start investing with a small amount?

Yes! Many LIC plans and mutual funds allow you to start with as little as ₹500 to ₹1,000 per month. The key is to start early.

Conclusion

The difference between savings and investment is the difference between surviving and thriving. While saving protects your present, investing secures your future. For every Indian family, the journey toward financial independence begins with a single step of disciplined planning.

Don't let your hard-earned money sit idle. Make it work for you. By balancing the importance of savings with the benefits of investment, you can ensure that a lack of funds never compromises your family’s dreams.

Need Help with Your Financial Journey?

Ready to create a roadmap for your family's future? Whether you need help with financial planning, understanding LIC policies, or choosing the right investment options, we are here to guide you.

Contact Nila Safe Life Solutions today for a free consultation.

Sundari S Mahila Career Agent – LIC Tindivanam Phone / WhatsApp: 9865822106

Website: www.nilasafelife.com

Get expert guidance to choose the right life insurance plan.

Nila Safe Life Solutions

Helping Indian families make smart financial decisions through the right insurance planning.

Trusted guidance. Honest advice.

Quick Links

Contact Me

📞 Call: +91 9865822106

Why Choose Me

✔️ Personalised insurance guidance

✔️ Support for claims & service

✔️ Focus on family financial security

🟢 Usually replies within 5 minutes on WhatsApp

“Insurance vangaradhu mukkiyam illa…

correct time-la vangaradhu dhaan mukkiyam.

© 2026 Nila Safe Life Solutions