Child Education Insurance Plans in India: Secure Their Future

Looking for the best Child Education Insurance Plans in India? Learn how to save for college, save on taxes, and ensure your child's dreams come true.

INSURANCE

Sundari S Mahila Career Adviser – LIC Tindivanam

4/14/20266 min read

Child Education Insurance Plans in India: The Ultimate Guide for Parents

Language: தமிழ் | English

Introduction

Every parent in India has one common dream: seeing their child graduate from a top university and lead a successful life. Whether it is becoming a doctor, an engineer, or a pilot, these dreams require a solid financial foundation. With the cost of education rising by 10-12% every year, a simple savings account is no longer enough.

This is where Child Education Insurance Plans in India come into play. These are not just insurance policies; they are specialised financial tools designed to ensure that your child’s educational journey never hits a roadblock, even if you are not around.

As a financial planner and LIC advisor, I have seen many families struggle because they started saving too late. In this guide, I will explain everything you need to know about choosing the right education savings plan in India.

Why Child Education Insurance Plans in India are Essential

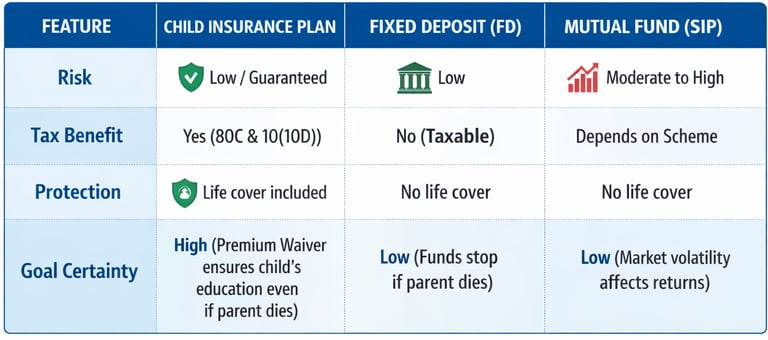

Many parents ask me, "Can't I just keep money in a Fixed Deposit?" While FDs are safe, they often fail to strike the "Education Inflation" in India. Here is why specialised child plans are superior:

1. Beating Education Inflation

The cost of a professional degree today might be ₹10 lakhs. In 15 years, that same degree could cost ₹40 lakhs. Child future-planning insurance helps you build a corpus that keeps pace with rising costs.

2. The Power of Compounding

When you start investing in a child's education early, your money grows exponentially. Even small monthly premiums can turn into a massive fund by the time your child turns 18.

3. Financial Security in Your Absence

This is the most critical feature. If something happens to the parent, the insurance company often waives future premiums and provides a payout to ensure the child’s education continues as planned. This is the true meaning of life insurance for child education.

Detailed Explanation of Child Education Insurance

A child insurance plan is a hybrid product. It combines the benefits of a savings plan with the protection of life insurance.

In India, these plans usually work in two phases:

The Accumulation Phase: You pay premiums regularly while your child is young.

The Payout Phase: The policy matures or provides "Money Back" instalments when your child reaches the age for higher education (usually 18 or 21).

These policies are designed to align with milestones in the Indian education system, such as completion of Class 12 and the start of post-graduation.

Key Features and Benefits of Child Insurance Plans

When looking for Child Education Insurance Plans in India, you should look for these specific benefits:

Maturity Benefit: A bulk amount paid at the end of the policy term to cover admission fees.

Premium Waiver Benefit (PWB): The most important rider. If the proposer (parent) passes away, all future premiums are waived, and the policy stays active. The child still receives the full maturity amount.

Partial Withdrawals: Some plans allow you to withdraw funds for school excursions or secondary education needs.

Tax Savings on Child Insurance Plans: Under Section 80C, the premiums you pay are tax-deductible. Furthermore, the maturity amount is usually tax-free under Section 10(10D) of the Income Tax Act.

Flexible Premium Payment: You can choose to pay monthly, quarterly, or annually based on your salary cycle.

Who Should Buy This Policy?

This policy is ideal for:

Young Parents: The earlier you start, the lower the premium and the higher the maturity.

Single Parents: To ensure their child’s future is legally and financially secure.

Salaried Employees: Who want a disciplined way to save for long-term goals.

Grandparents who wish to gift their grandchildren a secure future.

Example Scenario: The Sharma Family

Let’s look at a typical Indian family example.

Mr Rajesh Sharma is a 30-year-old software engineer in Tindivanam. He has a 2-year-old daughter, Diya. Rajesh wants Diya to have ₹25 lakhs for her higher studies when she turns 18.

He invests in one of the Child Education Insurance Plans in India with a Premium Waiver Benefit.

Annual Premium: Approximately ₹1.2 Lakhs.

Scenario A: Rajesh survives the term. At age 18, Diya receives the ₹25 lakhs plus bonuses, which covers her college fees.

Scenario B: Unfortunately, Rajesh passes away when Diya is 10. The insurance company immediately pays a Sum Assured to the family. More importantly, no more premiums need to be paid. When Diya turns 18, she still receives the full ₹25 lakhs for her education.

This "Double Benefit" is why child-specific plans are better than general savings.

Advantages and Disadvantages

Advantages

Guaranteed Funds: Unlike the stock market, many LIC child plans offer guaranteed additions and bonuses.

Disciplined Saving: It forces you to save for your child before spending on luxuries.

Loan Facility: Most policies allow you to take a loan against the policy if you face a financial emergency.

Disadvantages

Lock-in Period: You cannot withdraw the full amount in the first few years without a loss.

Moderate Returns: These are low-risk plans, so returns are stable but not as high as those of pure equity (though much safer).

Child Education Insurance Comparison: Insurance vs. Other Assets

How to Choose the Right Child Education Insurance Plan (Step-by-Step)

Choosing from the many Child Education Insurance Plans in India can be confusing. Follow these steps:

Please calculate the future cost; don't plan for today's costs. Add 10% inflation per year to estimate what college will cost 15 years from now.

Check for Riders: Always ensure the "Premium Waiver Benefit" is included. It is the heart of a child's plan.

Check the Insurer’s Claim Settlement Ratio: Always go with a trusted name like LIC, which has a legacy of honouring claims.

Identify the Milestones: Choose a policy that pays out when your child actually needs it (e.g., age 18 for Undergrad or age 21 for Postgrad).

Compare Plans: Look at child education insurance comparison charts to see which one offers the best bonuses.

Common Mistakes to Avoid

Waiting Too Late: Every year you delay increases your premium and reduces your final corpus.

Under-insuring: Many parents buy a policy for ₹5 lakhs, which won't even cover one year of engineering in 2040. Aim for at least ₹15-20 lakhs.

Insuring the Child Instead of the Parent: The insurance should be on the life of the breadwinner (the parent) to protect the child's future.

Ignoring the Inflation: A "big" amount today might be a "small" amount in 15 years.

Financial Advisor Tips

As a Mahila Career Advisor at LIC Tindivanam, I always tell my clients: "Your child’s education is a non-negotiable goal." Unlike a house or a car, you cannot take a "second chance" on your child's peak learning years.

Combine Plans: Sometimes, combining a money-back plan with an endowment plan provides liquidity at different stages of their education.

Start Small, but Start Now: Even if you can only afford ₹2,000 a month, start today. You can always buy an additional policy later when your income increases.

FAQ Section

1. What is the best age to start a child's education plan?

The best age is as soon as the child is born. Starting early allows you to pay lower premiums and benefit from long-term compounding.

2. Is LIC's child plan better than a Private Bank's plan?

LIC offers an unmatched sovereign guarantee and a very high claim settlement ratio, making it the most trusted choice for middle-class Indian families.

3. Can I withdraw money before maturity for a medical emergency?

Most Child Education Insurance Plans in India allow for partial withdrawals or policy loans after a certain period (usually 2-3 years).

4. Are the maturity proceeds taxable?

No, under current Indian tax laws (Section 10(10D)), the maturity amount of most life insurance policies is completely tax-free if the sum assured is at least 10 times the annual premium.

5. What happens if I stop paying premiums?

If you stop paying, the policy might lapse or become "paid-up" with reduced benefits. It is always better to choose an affordable child education policy that you can sustain over the long term.

Conclusion

Securing your child's future is the greatest gift you can give them. Child Education Insurance Plans in India offer the perfect mix of savings, growth, and most importantly, the "peace of mind" that your child will reach their goals no matter what life throws at them.

Don't leave your child's dreams to chance. Start planning today with Nila Safe Life Solutions.

Need help choosing the right LIC policy, term insurance, or financial planning for your family?

Contact Nila Safe Life Solutions today for a free consultation.

Sundari S Mahila Career Adviser – LIC Tindivanam

Phone / WhatsApp: 9865822106

Website: www.nilasafelife.com

Get expert guidance to choose the right life insurance plan.

Nila Safe Life Solutions

Helping Indian families make smart financial decisions through the right insurance planning.

Trusted guidance. Honest advice.

Quick Links

Contact Me

📞 Call: +91 9865822106

Why Choose Me

✔️ Personalised insurance guidance

✔️ Support for claims & service

✔️ Focus on family financial security

🟢 Usually replies within 5 minutes on WhatsApp

“Insurance vangaradhu mukkiyam illa…

correct time-la vangaradhu dhaan mukkiyam.

© 2026 Nila Safe Life Solutions