Atal Pension Yojana (APY) Guide: Benefits, Rules & How to Apply

Complete guide to the Atal Pension Yojana (APY scheme). Learn about eligibility, tax benefits, monthly contributions, and how to secure a guaranteed pension.

INDIAN GOVERNMENT SCHEMES

Sundari S Mahila Career Advisor – LIC Tindivanam

4/16/20266 min read

Atal Pension Yojana (APY): The Complete Guide to Your Retirement Security

Language: தமிழ் | English

Introduction

Retirement is a phase of life that everyone looks forward to, yet many fear. For those working in the unorganised sector in India—such as shopkeepers, farmers, or freelance workers—the lack of a steady monthly income after age 60 can be a major concern. This is where the Atal Pension Yojana (APY) comes into play.

At Nila Safe Life Solutions, we believe that every Indian deserves a dignified retirement. Understanding government-backed social security schemes is the first step toward financial freedom. In this pillar article, we will break down everything you need to know about this pension plan, from the registration process to the long-term benefits.

What is the Atal Pension Yojana (APY) Scheme?

The Atal Pension Yojana is a flagship social security scheme launched by the Government of India in 2015. It is specifically designed to provide a steady stream of income to workers in the unorganised sector who are not covered by any formal social security system.

Administered by the Pension Fund Regulatory and Development Authority (PFRDA) through the National Pension System (NPS) architecture, the APY scheme offers a guaranteed minimum pension of ₹1,000 to ₹5,000 per month after age 60, depending on your contributions.

Objectives of the Scheme

The primary objective of the APY scheme is to ensure that no Indian citizen has to worry about financial hardship in old age. The scheme focuses on:

Financial Inclusion: Bringing the "missing middle" into the fold of formal pension systems.

Longevity Risks: Protecting against the risk of outliving one's savings.

Encouraging Savings: Promoting a culture of small, regular savings among low-income groups.

Social Security: Reducing the dependency of senior citizens on their children or the state.

Key Benefits of Atal Pension Yojana

The Atal Pension Yojana is one of the most popular retirement tools in India for several reasons:

Guaranteed Pension: Unlike market-linked schemes, the pension amount is guaranteed by the Government of India.

Spouse Benefit: In the unfortunate event of the subscriber's death, the pension is automatically transferred to the spouse for their lifetime.

Return of Corpus: After the death of both the subscriber and the spouse, the entire accumulated pension wealth (the corpus) is returned to the nominee.

APY Tax Benefits: Contributions made under this scheme are eligible for tax deductions under Section 80CCD (1B) of the Income Tax Act, over and above the ₹1.5 lakh limit of Section 80C.

Low Cost: The administrative charges for managing APY are significantly lower than those for private pension plans.

Eligibility Criteria

To join the Atal Pension Yojana, an individual must meet the following criteria:

Nationality: Must be a citizen of India.

Age Limit: The entry age is between 18 and 40 years. Since the pension starts at 60, you must contribute for at least 20 years.

Bank Account: You must have a valid savings bank account linked with your Aadhaar and mobile number.

Taxpayer Status: As per the latest government rules (effective October 1, 2022), any citizen who is or has been an Income Taxpayer is not eligible to join the APY scheme.

Documents Required for APY Registration

The registration process is designed to be paperless and simple. You generally need:

Aadhaar Card: For identity and address verification.

Savings Bank Account Details: Including Account Number and IFSC code.

Mobile Number: For receiving transaction alerts and OTPs.

Nominee Details: Name and relationship of the person who will receive the corpus in case of death.

How to Apply (Step-by-Step APY Registration Process)

You can apply for the APY scheme through both offline and online channels.

Offline Method:

Visit your nearest bank branch or Post Office where you have a savings account.

Ask for the Atal Pension Yojana registration form.

Fill in your Aadhaar and mobile number.

Select your desired pension amount (₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000).

Provide the auto-debit authorisation so the premium is deducted automatically from your account.

Online Method (APY Online Application):

Log in to your bank’s Net Banking portal.

Look for the "Social Security Schemes" or "Insurance/Pension" section.

Select "Atal Pension Yojana."

The system will fetch your details from your bank record. Complete the remaining fields and submit.

Alternatively, you can use the e-APY portal provided by NSDL/CRA.

Contribution and Pension Details

The amount you contribute depends on two factors: your entry age and your target pension.

Entry at 18: If you start at 18 and want a ₹5,000 monthly pension, your monthly contribution is only about ₹210.

Entry at 40: If you join at the age limit of 40 for the same ₹5,000 pension, your monthly contribution rises to ₹1,454.

This highlights the importance of starting early. The sooner you start, the less you pay to secure your future.

Real-Life Example: The Power of Starting Early

Let’s look at Rahul, a 25-year-old self-employed graphic designer. He wants a guaranteed monthly income of ₹5,000 after he turns 60.

By enrolling in the Atal Pension Yojana today, Rahul’s monthly contribution would be approximately ₹376. Over the next 35 years, he will build a secure safety net. If Rahul waits until he is 35 to start, his monthly contribution for the same pension amount would jump to ₹902. By starting 10 years earlier, Rahul saves a significant amount of money while ensuring the same peace of mind.

Advantages and Disadvantages

Advantages:

Safety: 100% government-backed, zero risk of losing your principal.

Discipline: The auto-debit feature ensures you don’t forget to save.

Inclusivity: Even those with very low income can afford the ₹1,000 pension plan.

Disadvantages:

Fixed Pension: The maximum pension is capped at ₹5,000, which may be insufficient in future high-inflation environments.

Age Limit: Those aged 40 and above are not eligible to join the scheme.

Strict Exit Rules: Withdrawing before age 60 is only allowed in exceptional circumstances like terminal illness or death.

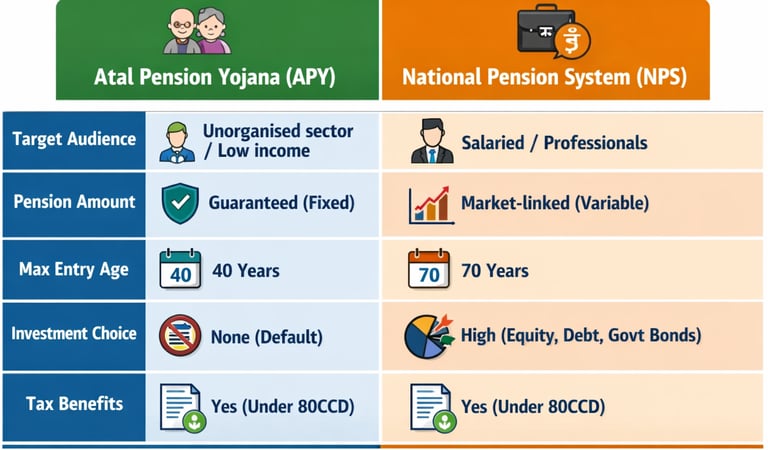

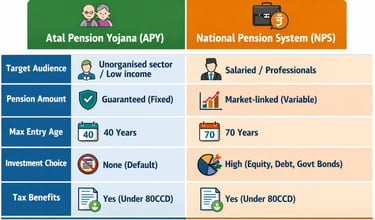

APY vs NPS Comparison

While PFRDA manages both,

They serve different needs:

Who Should Apply for This Scheme?

The APY scheme is ideal for:

Small business owners and shopkeepers.

Delivery partners, drivers, and domestic help.

Young earners looking for a low-cost, "set-and-forget" retirement plan.

Stay-at-home parents who want independent financial security in old age.

Important Tips Before Applying

Maintain Bank Balance: Ensure your savings account has enough funds on the auto-debit date to avoid small penalties.

Nominate Correctly: Always ensure your spouse is the primary nominee to allow for a seamless transition of benefits.

Upgrade/Downgrade: You can increase or decrease your pension amount once a year during April.

Check Status: Periodically check your APY PRAN (Permanent Retirement Account Number) statement online to ensure your contributions are being recorded.

Frequently Asked Questions (FAQs)

1. Can I have more than one APY account?

No. An individual may open only one Atal Pension Yojana account.

2. What happens if the subscriber dies before age 60?

The spouse has two options: continue contributing to the account for the remainder of the period or close the account and withdraw the accumulated corpus.

3. Are there any Atal Pension Yojana withdrawal rules for premature exit?

Generally, exit is only allowed at age 60. However, premature exit is permitted in case of the death of the subscriber or a terminal illness. In other cases of voluntary exit, only the subscriber's contribution and interest are returned (government co-contribution is withheld).

4. Can I apply for APY if I already have an EPF account?

Yes, you can apply as long as you are not an income taxpayer and fall within the 18-40 age bracket.

5. Is Aadhaar mandatory for APY?

Yes, Aadhaar is the primary document for KYC and is mandatory for enrolling in the scheme.

Conclusion

The Atal Pension Yojana is more than just a savings plan; it is a promise of a secure and dignified life for millions of Indians. By contributing a small amount today, you can ensure that your "Golden Years" are truly golden and stress-free.

Whether you are a young earner or a parent planning for the future, the APY scheme offers a simple, safe, and effective way to build a retirement corpus.

Need Help Securing Your Future?

Choosing the right retirement path can be confusing. Whether it is the Atal Pension Yojana, an LIC Policy, or a customised financial plan, we are here to help you make the right choice.

Contact Nila Safe Life Solutions today for expert guidance.

Sundari S

Mahila Career Advisor – LIC Tindivanam

Phone / WhatsApp: 9865822106

Website: www.nilasafelife.com

Get expert guidance to choose the right life insurance plan.

Nila Safe Life Solutions

Helping Indian families make smart financial decisions through the right insurance planning.

Trusted guidance. Honest advice.

Quick Links

Contact Me

📞 Call: +91 9865822106

Why Choose Me

✔️ Personalised insurance guidance

✔️ Support for claims & service

✔️ Focus on family financial security

🟢 Usually replies within 5 minutes on WhatsApp

“Insurance vangaradhu mukkiyam illa…

correct time-la vangaradhu dhaan mukkiyam.

© 2026 Nila Safe Life Solutions